China and Belarus present their relationship as high-quality cooperation under the Belt and Road Initiative (BRI). Since 2013, the relationship has been steadily upgraded from a comprehensive strategic partnership to an “all-weather comprehensive strategic partnership” in 2022, signaling long-term political alignment.

China and Belarus institutionalized this alignment through the Intergovernmental Cooperation Committee, established in 2014, a multi-level mechanism coordinating trade, investment, industrial policy, and logistics. This structure is common for China’s cooperation with BRI partners. Likewise, China has established special economic zones with several BRI partners, including Kazakhstan, Pakistan, and Egypt. The Great Stone Industrial Park in Belarus, however, is distinctive for its unusual proximity to the capital – a location that departs from the typical border- or port-based logic of Chinese overseas industrial zones. Alongside other bilateral projects, the Great Stone has incentivized the development of tailored legal rules – particularly since Belarus is not a WTO member.

China is Rising but Still Secondary

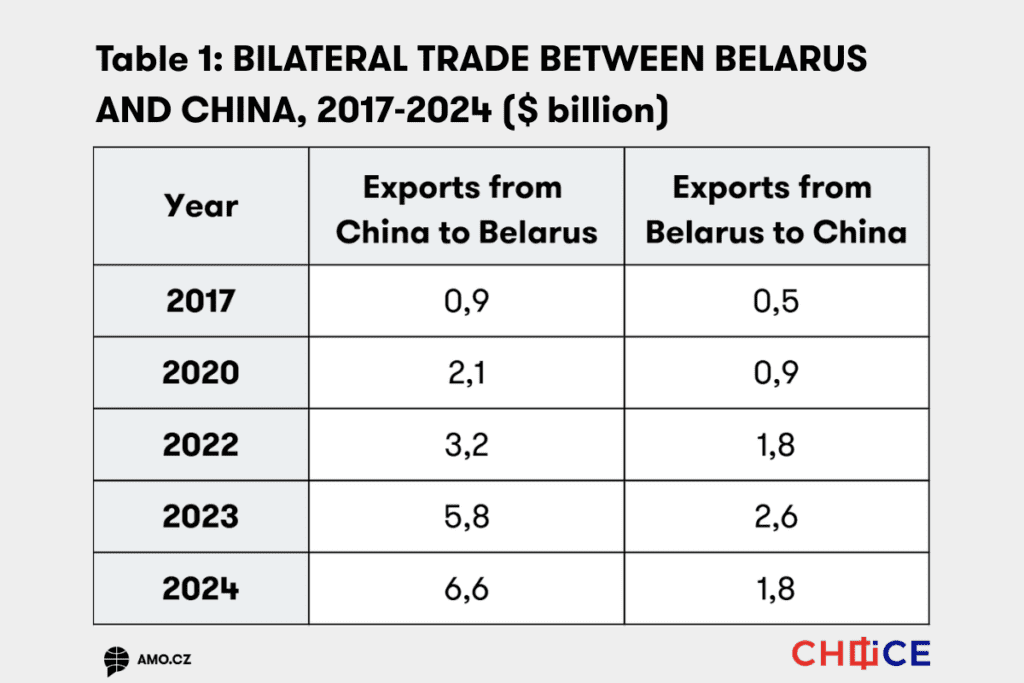

Bilateral trade between China and Belarus grew from a marginal base ($34 million in 1992) to a record $8.86 billion in 2025. Yet the relationship remains structurally asymmetric. Belarus exports mainly fertilizers, agricultural products, and wood; China exports vehicles, machinery, and electronics.

Even though China became Belarus’s second-largest trading partner in the early 2020s, imports from China accounted for only 9 percent of Belarus’s total imports in 2021 (imports from Russia constituted more than 56 percent), and exports to China represented 13 percent (exports to Russia 40 percent). In 2025, trade with countries not belonging to the Commonwealth of Independent States (CIS) totaled $31 billion, compared to $58 billion with CIS countries, reflecting Belarus’s dependence on this group. Moreover, prior to 2021, Belarus’s exports to Germany, the Netherlands, Lithuania, and Ukraine substantially exceeded current export levels to China. Despite the decline in bilateral trade in recent years, the EU has remained, in most years, Belarus’s second-largest trading partner. In 2024, Belarus imported goods worth $6.8 billion from the EU, while its exports to the Union amounted to approximately $1.2 billion.

Belarus’s total trade deficit deepened over time: according to official Belarusian data, $1.8 billion in 2021; $7.9 billion in 2024 and $9.3 billion in 2025, whereas IMF estimates a significantly larger deficit of $23 billion in 2024. By contrast, the trade balance with CIS countries remained positive, reaching $2.3 billion in 2025. In services, Belarus consistently recorded a trade surplus ($4.5 billion in 2021, $3.4 billion in in 2024), driven mostly by transport and ICT services, with Russia and the US as main destinations. Bilateral services trade with China mostly ran a deficit before 2022 (later data not available) and showed high volatility.

Foreign direct investment (FDI) mirrored this asymmetry. Between 2016-2019, Russia contributed 48.4 percent of FDI inflows, the UK 21.6 percent, and China only 1.3 percent, ranking ninth among Belarus’s investors. In terms of stock, Belarus’s total FDI stock amounts to $16.6 billion with a decreasing tendency. To date, China has provided around $5 billion in state-linked financing: only $461 million took the form of direct investment, while the remainder consisted of loans tied to the procurement of Chinese goods. In 2024, Belarus and China signed a memorandum specifically outlining procedures for using Chinese concessional government loansand establishing interagency cooperation on project proposals.

Despite the dramatic growth of China-Belarus trade, China plays an important but still secondary role compared to Russia and is unable for now to replace the European market for Belarusian exports.

Great Stone Industrial Park: Regulatory Enclave at the Centre of Belarus

Located near Minsk National Airport, the Great Stone China-Belarus Industrial Park is a flagship BRI project and the largest industrial park with Chinese participation outside China. It serves as a platform for selective investment, joint ventures, and technology-oriented production, while also anchoring China’s presence in Eastern Europe, albeit under sanction-constrained conditions.

The park operates under a special economic zone regime with a 50-year duration of preferential tax treatment. Residents benefit from a 10-year corporate income tax exemption (joint ventures until 2032), followed by a 50 percent reduced corporate tax rate, plus property and land tax exemptions. They also enjoy favorable labor migration rules and pay reduced social security contributions. Rather than a conventional free trade zone, the park represents a regulatory enclave with selective entry and controlled liberalization, prioritizing legal predictability over competition.

On paper, the park shows growth: resident companies increased from 68 in 2020 to 142 in 2024, spanning more than 15 countries – roughly half Chinese and one-third Belarusian. They work in machinery, e-commerce, AI and 5G, scientific research, and even traditional Chinese medicine. By 2023/2024, total committed investment in the park exceeded $1.3 billion. But trade figures within the park still show asymmetry: between 2019 and 2024, exports rose from $28 million to $156 million, yet imports increased from $58 million to $303 million.

China’s pragmatic approach faces obstacles: China criticizes Belarusian local content regulations, underdeveloped supply chains, and labor shortages, calling for a more market-oriented park and reforms of the state-run management.

Geopolitical Limits to the Gateway Strategy

More importantly, sanctions and geopolitics limit the park original “gateway to Europe” logic. After 2022, investment slowed, as some Chinese and Western investors postponed or cancelled projects (e.g. German Duisport). Two-way payment channels between China and Belarus were distracted, and transportation costs increased due to restrictions on transit imposed by Lithuania, Latvia, Poland, and Ukraine.

Ultimately, the park’s strategic value hinges on Belarus’s role as a transit hub. At present, Belarus remains China’s only land route, as political tensions with Lithuania and the Russia-Ukraine war constrain alternative paths to the EU market. However, China cannot fully exploit Belarus’s geographical advantage, since the planned international logistics terminal in the Great Stone Park, involving Chinese and Western companies to accelerate rail transport to Poland, Germany, and the Netherlands, is off the table. Nevertheless, the China-Europe Railway Express, a central component of the Belt and Road Initiative, began freight operations between Beijing and Minsk in May 2025.

Initially intended to serve European markets, goods from the Great Stone Park and other Chinese projects in Belarus flow mainly to Russia, given the single customs territory. But Russia shows limited interest in additional Chinese value-added production in Belarus, including vehicle assembly under the BelGee joint venture and related projects.

ATSI: The Next Level of Cooperation?

Signed in 2024 and in force since on January 1, 2026, the Agreement on Trade in Services and Investment (ATSI) has been presented as a qualitative shift in China-Belarus cooperation. The treaty establishes a free trade zone in the sense of Art. V of the WTO General Agreement on Trade in Services (GATS). China has similar agreements with other partners, but normally in a package with the establishment of free trade in goods.

ATSI uses a traditional positive-list approach: market access and national treatment obligations apply only to scheduled sectors. This choice reflects both parties’ preference for regulatory control, while liberalization remains sector-specific and focusing on commercially supportive sectors such as digital services, finance, logistics, and emerging technologies. The investment chapter covers market access, investor treatment, fund transfers, and investor-state dispute settlement. Unlike traditional bilateral investment treaties, it goes beyond protection of existing investments by promoting liberalization, such as allowing wholly foreign-owned enterprises in certain service sectors, and regulatory transparency.

Different from comprehensive free trade agreements, ATSI is primarily used as a rule-setting instrument to stabilize economic cooperation under sanction-constrained conditions. Its function seems to be to de-risk selective economic initiatives while ensuring control through legal frameworks. A telling illustration is the case of Wildberries – a Russian private e-commerce and logistics platform labelled by Xi Jinping as a key project under the BRI – which is now building a distribution center in the Great Stone Park.

ATSI also fits a broader Belarusian diversification logic. In 2025, Belarus signed and ratified a services andinvestment agreement with the United Arab Emirates (UAE), linked to a broaderEconomic Partnership Agreement between the Eurasian Economic Union and the UAE, suggesting Minsk seeks multiple “legal corridors” for services and capital under Western sanctions.

Governing Cooperation without Liberalization

China-Belarus cooperation challenges the classical assumption that economic integration precedes political alignment. Here, political alignment drives economic cooperation, and law becomes the mechanism translating alignment into predictable, controllable economic transactions.

Economic interaction is channeled through selective legal instruments rather than through broad market integration or trade liberalization. These instruments serve strategic purposes: they organize cooperation outside classical multilateral trade frameworks and help mitigate the effects of Western sanctions. Consequently, economic cooperation remains sector-specific, project-based, and reversible, prioritizing predictability over market openness. Both parties preserve strategic flexibility: China deepens engagement while managing sanctions exposure, whereas Belarus attracts investment while maintaining political control over key sectors. However, Belarus occupies a structurally weaker position due to its dependence on Russia, narrow industrial base, reliance on raw materials, and Western sanctions that restrict access to technology, capital, and markets.

As Belarus becomes increasingly isolated from Western markets, its reliance on China grows. China, in turn, approaches Belarus pragmatically – as a logistical corridor, a politically aligned partner, and a testing ground for non-Western models of economic cooperation. This asymmetry is reflected in divergent expectations. Belarus seeks greater Chinese investment, access to advanced technologies, and expanded export opportunities to offset sanctions, while retaining autonomy over its economic and social policies. China’s objective, by contrast, is to expand its own markets and strategic reach, using Belarus instrumentally during and after the Russia-Ukraine war.

Written by

Kateryna Zelenska

Dr. Kateryna Zelenska, LL.M., studied law in Ukraine and Germany and earned a PhD in international trade law from the University of Bremen. She was a Research Fellow at the WTO and worked at Brunswick School of Law (Ostfalia University of Applied Sciences). She now practices international trade law with a focus on the EU, Eastern Europe, and China.